Calculate within 1 minute if you can save money

Calculate within 1 minute if you can save money

- Insight in the money you are saving

- Non-binding

- Within one minute

Calculate now

The mortgage interest rate is still at an historic low but is slowly increasing. You can still reap the benefits by refinancing your mortgage. Use our Mortgage Update Calculator to check if you can reduce your monthly charges!

Calculate within 1 minute if you can save money

Calculate now

Refinancing your mortgage means you are moving your existing mortgage to a new mortgage. Often at a lower interest rate in order to save on your monthly charges. You can choose to stay with your current mortgage provider but it is often cheaper to change to a different supplier.

Paying a lower interest rate can save you hundreds of euros on a monthly basis.

Every month, you pay interest and (usually) pay off part of your mortgage. The mortgage interest rate is increasing but is still quite low! Something you can still benefit from.

The interest you pay has been agreed with your bank when you took out your mortgage. This doesn’t mean you are stuck with it. Refinancing your mortgage gives you the chance to benefit from a lower interest rate. This could save you hundreds of euros per month.

In 2010 the interest rate was 6%, these days it is often lower than 1.5%. Taking out a new mortgage means you could pay 75% less interest compared to 2010!

You are probably thinking: what about my penalty interest? This doesn’t have to be an issue!

When taking out a mortgage, you sign a contract for a fixed interest term. The fixed interest term represents the amount of years you need to pay interest. This is often capped at 10 or 20 years. Refinancing your mortgage means your bank will miss out on income. The penalty interest is used as compensation.

The amount of penalty interest depends on the following:

Luckily, it is often possible to include this penalty interest in your new mortgage. So you won’t have to pay a large sum of money at once.

As the interest on your mortgage is often tax deductable, you can also claim a large amount on your tax return.

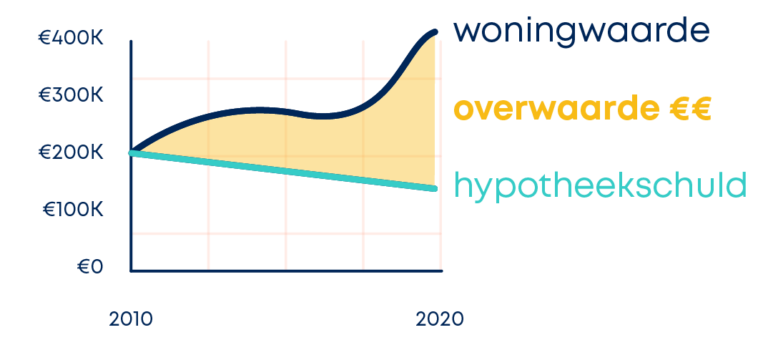

You probably have excess value on your property, thanks to the increase of housing prices. This means the value of your property is higher than your mortgage. Excess value can be a result of an increase of the value of the house, part of the mortgage has been paid off or a combination of both. Excess value on your property reduces the risk the bank is running and thus a lower interest rate.

If the penalty interest is too high, you could opt for rate averaging. You won’t change to a different mortgage, but pay an average on the current interest rate and your interest rate. You are charged penalty interest, however, this can be included in the new interest rate. As a result, your new interest rate won’t be as low as when chaging mortgage however, the fine to be paid is lower. Rate averaging is only possible at your existing mortgage provider, and cannot be done when changing to a different mortgage provider.

Vixx helps you make the right decision

We have your best interest at heart! We will sit down and look into the most economical solution available to you. Are you happy with the possible savings you can make and would you like Vixx to handle your new mortgage? This comes at a certain rate. The notary needs to be paid and Vixx charges a consultancy fee. These charges can often be included in your new mortgage and are tax deductable.

We will inform you of any possible charges before we get started, to avoid any surprises at a later stage.

Once we have established that you can save money, Vixx will search for the bank whose terms and conditions meet your personal requirements. We do this as an independent party. Your advisor will compare more than 35 banks to get you the best deal.

In the past, consultants were paid by the bank. This is no longer the case. As a customer, you get us involved to provide you with advise. We are here for you, not for the bank.

Are you curious to find out if you can reduce your monthly charges by financing your mortgage? Fill in the calculator in and find out if you can save money on your mortgage. It takes less than a minute!

If the mortgage calculator indicates you can save money, just leave your details or schedule an appointment with one of our consultants. We will look into your current situation and discuss your wishes during a non-binding meeting. We will provide you with tailor-made advice, as every situation is unique!

This meeting can take place where and when you prefer: at one of our offices, at your home or online.

After your meeting with the mortgage advisor, we will start searching for your most ideal mortgage! Which mortgage suits you best depends on your preferences and the conditions set by different banks. There are a lot of different mortgages, and they all have different terms and conditions:

- Interest rates

- Types of mortgage (linear, annuity, savings etc.)

- Fixed interest rate term

- Repayment

- And a lot more!

After we have looked into this for you, our mortgage advisor will provide you with a proposal regarding refinacing your mortgage.

When you are happy with this advice, Vixx will apply for a new mortgage proposal from the bank which meets your requirements. This could be your existing bank, or a different, cheaper bank.

Once the proposal is approved, Vixx will get cracking! We stay in touch with the bank and make sure all communication and necessary paperwork is dealt with accordingly. All you have to do is hand in the documents, Vixx takes care of everything else.

After the new mortgage contract has been signed, this needs to be registered at the notary. The notary will ensure your new mortgage is registered at the Dutch Cadastre, Land Registry and Mapping Agency and your old mortgage is no longer valid.

Any questions? Just get in touch. We look forward to talking to you!

Are you curious to find out if you can reduce your monthly charges by financing your mortgage? Fill in the calculator in and find out if you can save money on your mortgage. It takes less than a minute!

Ruud and Helen retired last year. They asked Vixx if they could save money on their mortgage, to make the most of their retirement.

Ruud and Helen had exces value on their property and were paying 5.3% interest. After talking to their advisor, they decided to reduce their monthly payments to pay off their mortgage. Because who are you doing it for if you are already retired?

Part of their mortgage is now interest-only, and the other part has an interest rate of only 1.4%. As a result, their monthly charges reduced considerably, giving them to chance to enjoy their retirement.

Pauline and Rachid would like to start a family. A bit more financial freedom would be more than welcome.

The fixed interest term of their mortgage expired after ten years. As a result of the increase in property values, their property fell into a different risk class compared to ten years earlier. This is because of the excess value on the property and the fact that the bank runs a smaller risk.

Vixx compared all offers and transferred the mortgage to a different bank. Paulin and Rachid are saving money, which they can use for starting a family!

Esméé bought an apartment in Amsterdam eight years ago at a fixed interest term of 20 years. She didn’t expect to be able to benefit from the low interest rate as she would have to pay a considerable penalty interest.

After talking to Vixx she realised it could be possible! Due to her property increasing in value and paying off part of her mortgage, there was a considerable excess value on her property.

Vixx ensured Esméé increased her mortgage to pay off the penalty interest. Her mortgage falls under a different risk class. She benefits from the lower interest rate and is using spread payments to pay off her fine. Money she would otherwise spend on the high interest rate of her existing mortgage.

In order to protect our clients’ privacy, these profiles are fictional characters based on actual results.

An experienced consultant who spends time looking into your personal circumstances, will be able to get the most out of your mortgage. We handle tens of mortgages on a monthly basis, and therefore have extensive knowledge on the various options. The mortgage market holds no secrets for us, enabling us to provide you with the best advice available. We compare mortgage suppliers, making sure you get the best deal.

Refinancing your mortgage might be interesting when your current interest rate is higher than the interest rate provided by mortgage lenders. Also, your long-term profit should be higher than the fine you pay to get out of your fixed-interest rate period. The sum of this fine depends on your personal situation.

The costs depend on your personal situation. The charges include a consultancy fee and possibly a fine for settlement of the fixed-interest rate period. It is possible to include this fine when financing your new mortgage. It is difficult to establish the exact costs without closely looking at your personal circumstances, please get in touch and we will provide you with an estimate free of charge.